FADA Releases Apr’25 Vehicle Retail Data

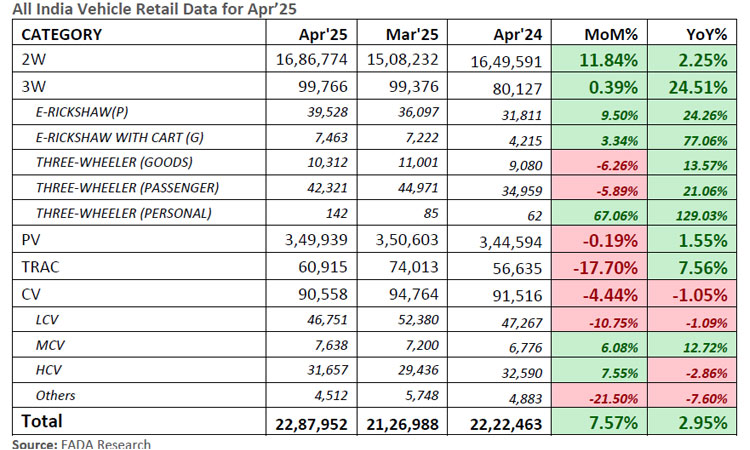

Reflecting on April 2025 auto-retail results, FADA President Mr. C S Vigneshwar noted: “The new financial began on a modest note as overall retails in April managed to grow by 3% YoY. All categories except CV closed in the green, with 2W, 3W, PV and Trac up 2.25%, 24.5%, 1.5% and 7.5% respectively, while CVs declined by 1%. With the tariff war paused, stock markets staged a sharp pullback—alleviating investor concerns—and customers thus leveraged Chaitra Navratri, Akshay Tritiya, Bengali New Year, Baisakhi and Vishu to complete purchases, helping April end on a positive note.

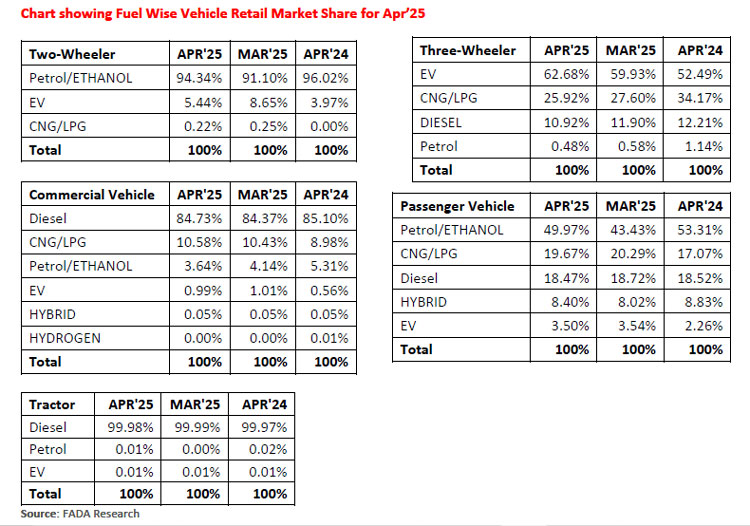

2W retail volumes demonstrated a resilient up-cycle—growing 2.25% YoY and accelerating 11.84% MoM underscoring a stable demand environment amid mixed headwinds. Dealers reported buoyant enquiry growth in rural areas post-Rabi harvest, driven by strong crop yields, healthy reservoir levels and a favourable monsoon outlook, while wedding-season tailwinds sustained rural offtake. Urban demand remained robust, supported by new-model introductions, although elevated financing costs and OBD2B-linked price adjustments posed isolated bottlenecks.

Despite limited model introductions, the PV segment registered a 1.55% YoY increase alongside a marginal 0.19% MoM decline. This performance reflects a discount-led market and elevated inventories—approximately a 50-day supply—amid cautious consumer sentiment that tempered enquiry-to-sale conversions. Sustained SUV demand underpinned volumes even as entry-level customers remained cautious, underscoring the need for OEMs to recalibrate production and reduce stock levels to mitigate deeper discounts and carrying costs at dealerships. FADA continues to advocate a 21-day inventory norm at dealerships to enhance market responsiveness and cost efficiency.

April’s CV segment faced a 1.05% YoY decline and a 4.44% MoM contraction following OEM-led price increases against stagnant freight rates and fleet utilisation. Dealer feedback highlights that advance purchases in March resulted in elevated carryover stocks, while holiday calendars dampened fresh enquiries and delayed conversions— particularly in the SCV cargo category, where price and product gaps have weighed heavily. Conversely, the bus segment exhibited resilience, underpinned by strong school-transport and staff-mobility demand. Although financing availability remains broadly stable, enhanced support for first-time users will be critical to reignite

momentum.”