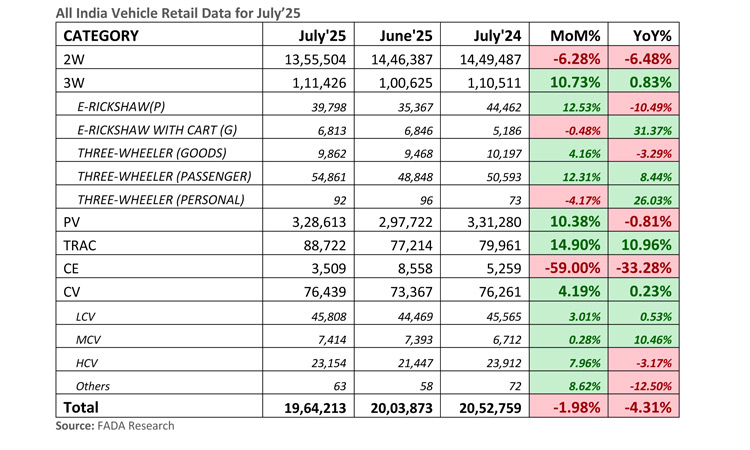

FADA Releases July’25 Vehicle Retail Data

Reflecting on July 2025 Auto Retail results, FADA President Mr. C S Vigneshwar said: “After three consecutive months of growth, India’s auto retail sector applied the brakes in July, with overall retails declining by 4.31% YoY. This pullback largely stems from a high-base effect in July 2024, when an extreme heat wave was immediately followed by excessive rainfall, constraining volumes before a rebound later that month.

Segment‐wise, 3W, Trac and CV achieved growth of 0.83%, 10.96% and 0.23% YoY respectively, whereas 2W, PV and CE contracted by 6.48%, 0.81% and 33.28% YoY.

In the 2W space, July saw a 6.48% YoY decline and a 6.28% MoM drop, as crop-sowing activities and prolonged heavy rains dampened rural footfalls more sharply than urban demand. Dealers are nevertheless confident of a post-monsoon uptick, with several purchase decisions deferred to August ahead of the festive season—making strategic stock alignment and focused rural–urban engagement imperative for reviving momentum.

The PV segment contracted by 0.81% YoY even as volumes surged 10.38% MoM, driven by robust rural demand. The Aashaada period and auspicious delivery days, combined with targeted schemes, new-model introductions and aggressive rural marketing, powered hinterland sales that picked up decisively towards month-end. Urban demand, however, remained muted due to low enquiry and restrained customer sentiment. With inventory levels steady at around 55 days, calibrated discounting, streamlined finance facilitation and intensified urban outreach will be crucial for sustaining festive-season growth.

CV posted a modest 0.23% YoY increase and a 4.19% MoM uptick, led by urban momentum. Dealers cited new-model launches, aggressive marketing support, bulk institutional orders and timely stock availability as key drivers, alongside targeted schemes that bolstered school-bus volumes. In contrast, rural haulage demand remained fragmented amid heavy rainfall, seasonal softness in cement, coal and construction logistics, and slower financier disbursements, prompting many buyers to defer purchases to the post-monsoon period.

Finally, the Trac segment delivered robust performance, with volumes up 10.96% YoY and 14.9% MoM. The timely release of enhanced agricultural subsidies and favourable monsoon rains—together with strengthened rural liquidity—spurred a marked increase in purchase intent. This resilience underscores the pivotal role of policy interventions in sustaining agri-rural demand.”

Chart showing Vehicle Retail Data for July’25

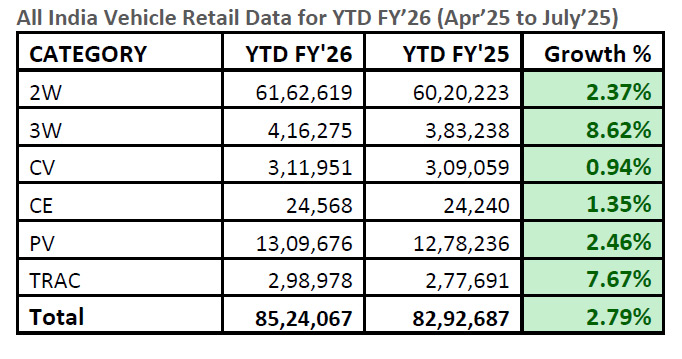

All India Vehicle Retail Data for July’25

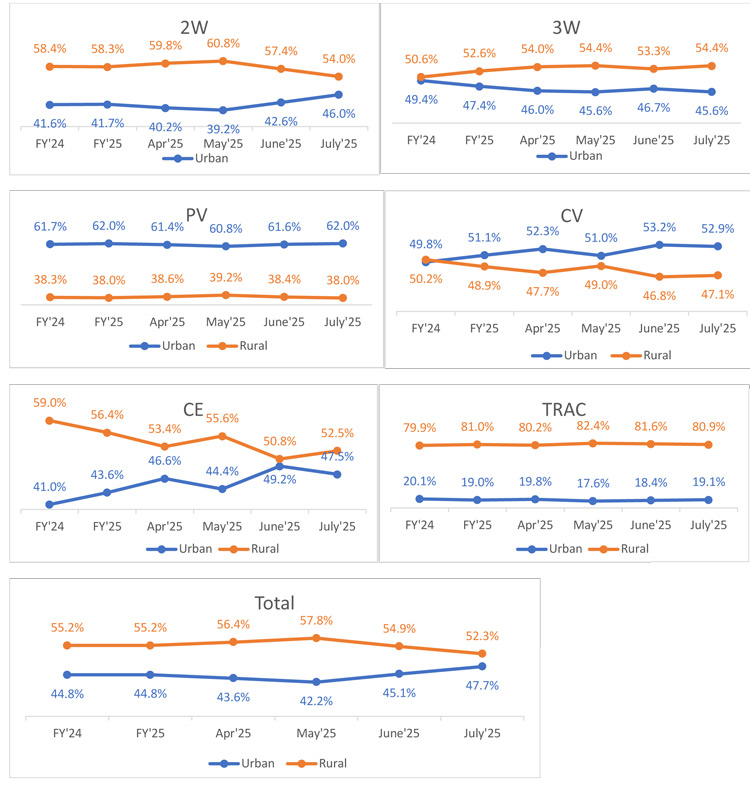

All India Vehicle Retail Strength Index for July’25 on basis of Urban & Rural RTOs.